Byte # 54: Why I’m Studying Schneider Electric (SBGSY): The Quiet Giant Powering the AI Era

Hello and Welcome all to this week’s byte.

For the third consecutive week, I'm staying focused on a theme that continues to dominate both my research and the markets: electrification.

Much has been written about AI's "iPhone moment." Investors are understandably focused on GPUs, semiconductors, cloud providers, and the companies building the models. But behind every AI breakthrough sits a less glamorous yet absolutely essential layer of infrastructure: power, energy management, cooling, automation, and grid modernization.

AI isn't just a computing story. It's increasingly becoming an electricity story.

A recent UN Trade and Development (UNCTAD) report projects the artificial intelligence market will grow from $189 billion in 2023 to $4.8 trillion by 2033 - a 25-fold increase in just one decade. Supporting that growth will require a massive expansion of data center infrastructure. According to the International Energy Agency, global data center electricity consumption is expected to double by 2030.

The challenge is that AI data centers consume significantly more power than traditional facilities. High-density GPU clusters are pushing power delivery and cooling systems to their limits, making intelligent energy management, advanced power distribution, and liquid cooling critical components of the AI stack.

This is where Schneider Electric quietly enters the picture.

While it rarely generates the same headlines as Nvidia or the hyperscalers, Schneider sits at the intersection of several of the most important long-term trends shaping the global economy: electrification, automation, energy efficiency, and now AI infrastructure.

In many ways, Schneider has become one of the foundational enablers of the AI era.

Company background: A 180‑year reinvention story

Founded in 1836 in France, Schneider Electric began in steel and armaments and has spent nearly two centuries methodically reinventing itself into a global leader in:

Energy management systems

Industrial automation

Building efficiency and controls

Data center power & cooling

Grid and microgrid solutions

Today, Schneider operates in 150+ countries, with a portfolio that touches almost every node of modern electrical and digital infrastructure.

This is not a hype‑cycle company. It is a mission-critical infrastructure platform that has spent decades positioning itself for many of the secular trends now reshaping the global economy.

How Schneider fits the AI infrastructure story

As AI buildouts accelerate, power availability is emerging as one of the industry's biggest bottlenecks.

Training larger models requires more compute. More compute requires more servers. More servers require more power, cooling, and energy management. The result is a multi-year infrastructure investment cycle that extends far beyond semiconductors.

Schneider sits right at this intersection:

EcoStruxure Data Center: an integrated platform combining power management, cooling, racks, and data center infrastructure management software.

Liquid cooling: strengthened by acquisitions like Motivair, allowing Schneider to address the growing demand for high-density AI workloads.

Microgrids & grid‑interactive solutions: helping large AI campuses manage increasingly volatile and power-intensive loads.

Building & industrial automation: enabling efficient, software‑defined infrastructure around those data centers

Schneider's position in the AI ecosystem is further strengthened by its partnership with NVIDIA. The two companies are co-developing power systems, liquid-cooling technologies, and high-density rack architectures designed for next-generation AI and giga factories.

As a result, research firms increasingly identify Schneider and Vertiv as the two global leaders in data center physical infrastructure, with Eaton close behind.

Understanding Schneider's Business

Schneider’s portfolio is broadly organized into two major engines:

1. Energy management (€33.1B in FY25 | ~82% of Revenue)

This is the company's largest business and includes:

Low- and medium-voltage switchgear

UPS and power quality systems

Data center power and cooling infrastructure

Building management and energy efficiency solutions

Residential and commercial electrical distribution

The segment generated €8.0 billion in revenue during Q1 FY26, representing 12.8% organic growth.

Historically, the business has delivered steady mid-single-digit organic growth while benefiting from margin expansion driven by software, services, and integrated solutions.

Today, AI-related data center demand is becoming an increasingly meaningful growth driver, with data-center-related revenue growing faster than the broader business.

2. Industrial Automation (€7.0B in FY25 | ~18% of Revenue)

This segment includes:

Factory and process automation

Motion control and robotics

Industrial software through AVEVA

Digital twins and OT/IT convergence solutions

The segment generated €1.7 billion in Q1 FY26 revenue and grew 4.4% organically.

While smaller than Energy Management, Industrial Automation provides exposure to several long-term trends, including digital factories, industrial software, electrification, and manufacturing modernization.

What stands out to me is that both segments are tied to the same secular forces Schneider has been discussing for years: electrification and digitization.

AI doesn't change the story. It accelerates it.

How Schneider compares to Eaton and Vertiv

When investors think about AI infrastructure beyond semiconductors, Schneider, Eaton, and Vertiv are increasingly appearing in the same conversation.

However, each company offers a different investment proposition.

Vertiv is the pure-play AI infrastructure story. Its business is heavily concentrated in data center power and thermal management, making it one of the most direct beneficiaries of AI spending.

Eaton is a diversified electrical leader with significant exposure to power distribution, Uninterruptible Power Supply (UPS) systems, and growing capabilities in liquid cooling.

Schneider sits somewhere between the two.

Unlike Vertiv, Schneider's future does not depend entirely on data centers. Unlike Eaton, Schneider combines energy management, industrial automation, software, building controls, and AI infrastructure under one platform.

This gives investors exposure to multiple growth engines rather than a single theme.

Market position

Schneider and Vertiv are now neck‑and‑neck leaders in data center physical infrastructure (power + cooling), separated by only a fraction of a percentage point in global market share.

Eaton is a top‑tier player in electrical and power distribution, with growing data center exposure and strong partnerships in liquid cooling.

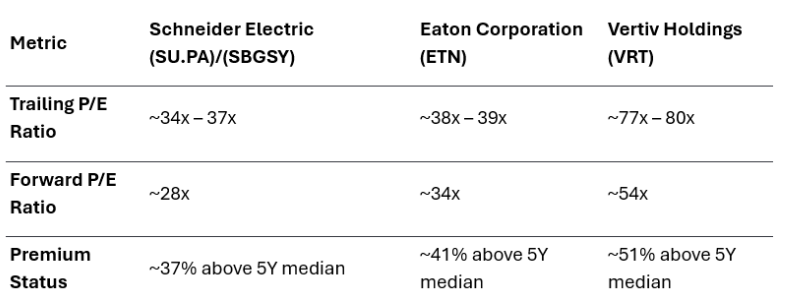

From a valuation perspective, Vertiv commands the highest multiple due to its concentrated AI exposure and rapid growth profile. Eaton typically trades at a premium reflecting its quality industrial characteristics and strong execution.

Schneider often occupies what I consider the "quality compounder" category: a premium valuation relative to traditional industrials, but often more reasonable than pure AI infrastructure names.

The way I frame the valuation looking at the multiples above:

Vertiv = high‑beta AI infrastructure growth

Eaton = blue‑chip electrical compounder

Schneider = platform play on electrification + AI + automation, with a more balanced risk/return profile

Fundamentals and management outlook

What makes Schneider particularly interesting to me as a long-term compounder is the quality of the business model.

The company benefits from:

Mission-critical products with meaningful pricing power

High switching costs and long qualification cycles

Diversified exposure across data centers, utilities, industrials, buildings, and residential markets

Strong free cash flow generation

Disciplined capital allocation

Increasing software and recurring revenue streams

One data point I found particularly interesting came from Dell'Oro Group, which noted that recent revenue growth across power and cooling vendors has been driven not only by higher volumes but also by higher average selling prices.

In other words, companies such as Schneider, Eaton, and Vertiv have demonstrated the ability to pass through inflationary pressures while maintaining demand...evidence of genuine pricing power.

Management's long-term message has remained remarkably consistent:

Electrification is a multi-decade trend

AI is increasing power density and electricity demand

Buildings, factories, and data centers must become digitally managed energy systems

Grid constraints and sustainability targets will require more intelligent infrastructure solutions

Looking ahead, Schneider estimates its addressable market could reach €600 billion by 2030, growing at approximately 6%-7% annually.

Over the next five years, management is targeting:

7%-10% annual revenue growth

15%-20% returns on capital

100% free cash flow conversion

That cash generation supports continued dividend growth, share repurchases of up to €3.5 billion, and ongoing investment in growth opportunities.

To me, this reinforces an important point: Schneider is not simply betting on one AI cycle. It is positioned for a broader transformation in how energy is generated, distributed, managed, and consumed.

The Risks

No investment thesis is complete without considering what could go wrong.

Valuation: Schneider currently trades at approximately 34.7x earnings versus a five-year average multiple of roughly 25.4x. Even after incorporating expected earnings growth, the forward P/E remains elevated near 28x. Investors are clearly paying a premium for the company's AI exposure, electrification positioning, and software-driven growth profile.

Cyclicality and capex sensitivity: While secular trends are strong, Schneider is still exposed to macro cycles in construction, industrial capex, and data center spending. A pause in hyperscaler build‑outs or a broader slowdown could pressure growth.

Competition from Vertiv and Eaton: In data center physical infrastructure, Schneider is in a real knife‑fight with Vertiv and Eaton for share, especially in liquid cooling and high‑density power. Execution missteps, pricing pressure, or slower innovation could erode its edge.

Execution on AI‑era technologies (especially liquid cooling): The market is moving fast toward direct‑to‑chip and advanced liquid cooling. Schneider has been active (e.g., Motivair acquisition), but this is a space where technology and partnerships matter. Falling behind here would blunt its AI upside.

Regulatory and ESG expectations: As a global energy and infrastructure player, Schneider is exposed to evolving regulations, ESG scrutiny, and policy shifts around grids, emissions, and building standards. These can create both opportunities and compliance costs.

FX and geographic complexity: With operations in 150+ countries, currency swings and regional political risks are part of the package.

For me, these risks are real but understandable - they’re the kind of risks you expect when you’re investing in a global infrastructure platform, not a speculative story stock.

Why Schneider Has Earned a Place on My Watchlist

What attracts me most to Schneider Electric is the combination of multiple long-term growth drivers within a single business.

Investors gain exposure to:

AI infrastructure through data center power and cooling

Electrification through grids, EVs, buildings, and utilities

Automation through factories, industrial software, and digital operations

At the same time, the company possesses many of the characteristics I look for in long-duration compounders:

Pricing power

High returns on capital

Diversified revenue streams

Strong cash generation

Increasing software exposure

In a world where AI is pushing global electricity demand into an entirely new regime, I want exposure not only to the chips that enable AI, but also to the infrastructure that makes those chips useful.

And that is exactly where Schneider Electric appears to be quietly building an advantage.

Let me know what you think. Is Schneider Electric a company that could earn a core position in your portfolio?

As always, this isn't a recommendation to buy or sell...it's about revisiting the process and stress-testing whether the original thesis still holds.

Keep investing smarter 😊

Cheers,

Pooja