Byte # 53: The AI Energy Bottleneck

Dear Readers,

Hello and Welcome to this week’s Byte…which is an extension of my last piece, Demand Is Surging. The Grid Isn’t Ready.

I want to continue this conversation because I want you to understand one simple idea: electricity is the fuel of the AI economy.

The energy crisis is real and growing. Geopolitical disruptions are tightening supply at the same time AI and electrification are pushing demand higher.

According to the International Energy Agency (IEA), the Middle East conflict triggered one of the largest oil supply disruptions in history, temporarily removing roughly 8 to 10 million barrels per day from global supply.

Here is another reminder from Bloomberg: the world is underestimating how long the impact of the Iran war will last on global liquefied natural gas supply, according to Australia’s top exporter of the fuel. You may want to read the full article here.

At the same time, hyperscalers are deploying extraordinary amounts of capital into AI infrastructure. Roughly $700 billion in spending is flowing into the physical backbone behind AI - massive industrial facilities the size of football fields, gigawatt-scale power systems, advanced cooling infrastructure, and the transmission networks required to support them.

That brings us to one of AI’s biggest bottlenecks: generating enough reliable electricity.

Renewables will remain an important part of the energy mix, but only to a point. Solar panels do not produce power at night, and wind turbines only work when the air is moving.

That leaves natural gas, hydroelectric power, and nuclear energy as the most reliable large-scale power sources capable of supporting AI demand. Since most large-scale hydroelectric capacity in North America has already been developed, the two most important incremental power sources for the next decade are likely to be natural gas and nuclear.

This takes me back to a point I’ve emphasized repeatedly in previous Bytes: Energy remains one of the most important areas to own.

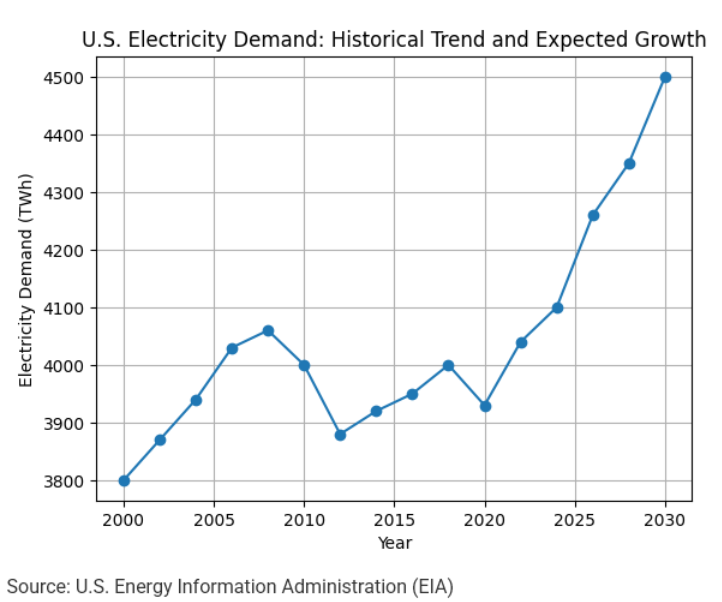

If AI truly is the next great industrial revolution, then U.S. electricity consumption is expected to rise meaningfully over the coming decade. Some projections suggest electricity demand could increase by 15% to 20% by 2030.

If you look at the chart above, electricity demand was relatively sluggish until 2020, and then it began to surge. This is the largest sustained increase in power demand the country has seen since the post-World War II industrial boom.

So where is this power going to come from?

Natural Gas: Natural gas remains one of North America’s greatest competitive advantages. The region can generate relatively low-cost electricity using abundant U.S. natural gas reserves, supported by the largest pipeline infrastructure network in the world.

This is also why I previously called out companies such as Headwater Exploration (CDDRF), ONEOK (OKE), Enterprise Products Partners (EPD), MPLX LP (MPLX), Brookfield Infrastructure (BIP), and Brookfield Renewable (BEP). The original thesis was never dependent on geopolitical conflict. Energy demand was already accelerating due to AI, electrification, and industrial reshoring. The Middle East disruptions have simply intensified an existing trend.

These businesses can potentially benefit from both dividend income and long-term infrastructure demand tied to AI growth.

In my last Byte, I also mentioned GE Vernova. Its natural gas turbine order book is now stretched into multi-year wait times and reportedly sold out through 2028 - another sign of how rapidly power demand is rising.

It is also worth remembering that while oil remains the world’s largest energy source, however, natural gas is cleaner and cheaper and more scalable for electricity generation. That gives North America a meaningful competitive advantage in supplying low-cost energy to the world.

Nuclear: Nuclear energy has re-emerged as a critical part of the conversation.

After moving from a historic boom to a decade-long bear market, uranium has entered a new structural bull market driven partly by AI-related electricity demand.

What is particularly notable is that large technology companies are no longer simply discussing AI growth...they are actively securing future power supply.

Over the last two years, hyperscalers including Meta, Amazon AWS, Alphabet, Microsoft, and Oracle have announced nuclear-related partnerships, power purchase agreements, and investments tied directly to long-term electricity needs.

That tells us something important: AI has also become an energy infrastructure story as much as a technology story.

So where do I still see opportunity today, even after many infrastructure-related stocks have already moved sharply higher?

Here are two stocks that I find worthy of attention:

EQT Corp (EQT) - EQT is an independent natural gas producer focused on the Marcellus and Utica shales in the Appalachian Basin. It operates across production, gathering, and transmission.

EQT looks attractively valued today, has a stronger balance sheet, and benefits from a favorable global gas backdrop tied to Middle East disruptions. It is one of the largest natural gas producers with its own midstream infrastructure and one of the lowest-cost operators in Appalachia. That puts it in a strong position for LNG growth and data center demand, although infrastructure timing and commodity volatility remain key risks.

Constellation Energy (CEG) – Constellation is now one of the most strategically important electricity platforms in the United States. Following its acquisition of Calpine in January 2026, the company became the nation’s largest electricity producer, with a diversified portfolio spanning nuclear, natural gas, hydro, wind, solar, geothermal, cogeneration, and battery storage.

Its nuclear fleet is increasingly becoming strategic AI infrastructure.

Meta recently signed a 20-year power purchase agreement tied to the full output of the Clinton Clean Energy Center, while Microsoft supported the restart of the Crane Clean Energy Center through another long-duration agreement.

These deals matter because they demonstrate that hyperscalers are willing to underwrite long-term, reliable, clean electricity at scale.

That improves earnings visibility, strengthens returns on nuclear assets, and supports a stronger valuation framework for companies capable of supplying reliable baseload power.

Constellation shares remain volatile and have pulled back meaningfully from prior highs. Investor sentiment across the electricity space has cooled somewhat this year following significant gains across many AI infrastructure names.

However, given the broader macro backdrop and Constellation’s evolution into a large-scale power platform, the recent pullback could create an interesting entry point for long-term investors.

The biggest risk, in my view, is timing. AI-related power demand may ultimately take longer to translate into earnings growth than the market currently expects.

I hope you found this conversation useful and I’ll see you next week.

As always, this isn’t a recommendation to buy or sell-it’s about revisiting the process and stress-testing whether the original thesis still holds.

Keep investing smarter😊

Cheers,

Pooja