Byte # 49: If This Is “Day 1”… How Big Can Amazon Get?

Dear Readers,

Every now and then, a shareholder letter forces you to pause...not because of what’s happening today, but because of what could happen next.

That’s how I felt reading Andy Jassy’s latest letter released on April 9, 2026.

It doesn’t read like a mature company defending its position. It reads like a company still building its next act.

Where Amazon Stands Today (as of 12/31/25)

Amazon is already operating at a scale that’s hard to fully grasp:

Market Cap: ~$2.47T

Revenue: ~$717B

Revenue by Segment: Retail/E-commerce ~72.5%; Amazon Web Services (AWS) ~18%; Advertising ~9.5%

AWS: The profit engine, generating ~57% of total operating income with ~35% operating margin.

Growth Engine: AWS and Advertising grew ~20% and ~22% YOY, respectively

Overall net income grew by ~31% YoY as of December 31, 2025.

But the real story isn’t the size. It’s where the next layers of growth come from.

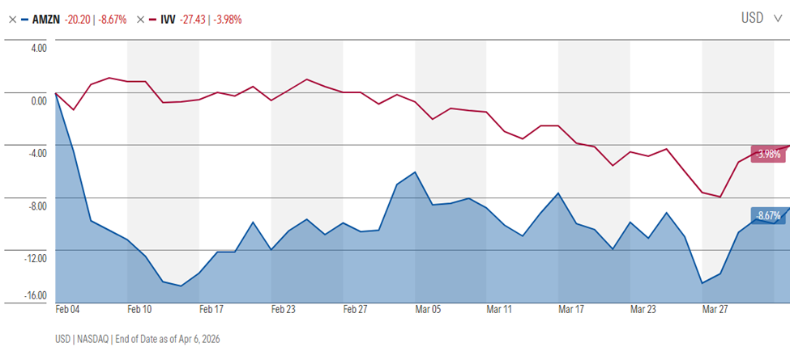

From the day of the earnings announcement for FY ended December 31 2025, to the day before Jassy's letter, Amazon's stock dropped ~9%, a notable underperformance over a short period.

The stock reached a low of $199 on March 27, before closing at $208.07 on March 31. Much of this weakness was driven by investor concerns around Amazon’s ~$200B capex commitment for 2026.

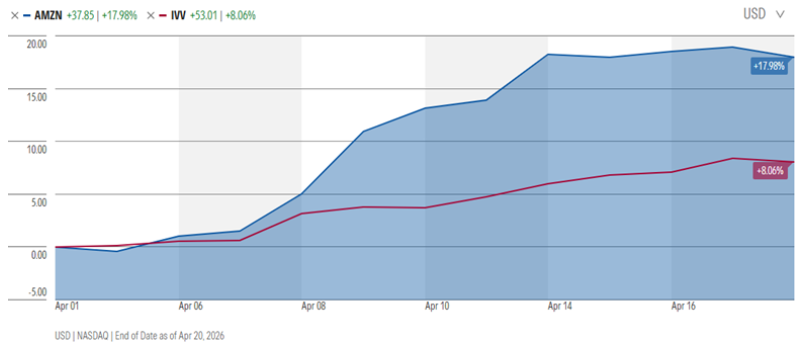

Since the letter’s release and some easing in geopolitical tensions…the stock has rebounded meaningfully, rising ~18% versus ~8% for the S&P 500 (IVV) between April 1 and April 20, 2026.

This is where the CEO’s letter becomes important.

It clearly reinforces that inventing the next inflection point has always been central to Amazon’s growth...and that philosophy continues today across AI, robotics, space, and logistics.

The 6 Growth Engines Jassy Is Quietly Building

1. AI + AWS (The Next AWS?)

Jassy is crystal clear: AI is a once-in-a-generation platform shift.

“Three years after AWS launched commercially, it had a $58 million revenue run rate. Three years into this AI wave, AWS’s AI revenue run rate is over $15 billion in Q1 2026 (nearly 260 times larger than AWS at that same point)...and ascending rapidly.”

AI revenue already at a $15B+ annual run rate

AWS remains the backbone of enterprise AI - In 2025, AWS added ~3.9GW of power capacity and expects to double it by 2027...yet demand still exceeds supply

AI could help scale AWS into a $600B business by 2036 (~17% CAGR)

2. Custom Silicon (Underrated Margin Driver)

Amazon is not just consuming compute...it’s building it.

“If our chips business were standalone… our annual run rate would be ~$50 billion. There’s so much demand for our chips that it’s quite possible we’ll sell racks of them to third parties in the future.”

Trainium, Graviton, Nitro chips

Already $20B+ run-rate business and growing triple digit percentages YoY

What does this mean for the business:

Reduces dependency on others’ chips for inference (e.g. NVDA)

Lower costs for customers

Expands AWS margins further

3. Advertising (The Silent Giant)

Often overlooked, but increasingly important:

High-margin, fast-growing

Built on top of Amazon’s commerce intent data

Still under-monetized relative to peers

This could quietly become one of Amazon’s most profitable segments.

4. Robotics (The Efficiency Flywheel)

Accelerated by the Kiva acquisition in 2012 and years of investment:

1M+ robots in fulfillment network

Faster delivery → better customer experience → more Prime usage

“We’re still in the early stages of how we’ll leverage robotics. Wherever we can leverage our scale and real-time feedback loop from so many robots in our fulfillment network to build robotics solutions for other industrial and consumer customers, we’ll explore doing so.”

This is not just cost optimization. It’s a moat that’s getting deeper every year.

5. Capex at scale (~$200B in 2026)

Amazon is being completely transparent about its investment cycle:

“We are willing to make large capex investments and endure short-term FCF headwinds…”

Significant monetization expected in 2027–2028

Classic Amazon playbook: heavy investment → skepticism → eventual payoff

6. Optionality Bets (The “Hidden Upside”)

Jassy highlights multiple long-duration bets:

Amazon Leo (satellite network) – stronger performance at lower cost and its seamless integration with AWS.

Healthcare

Grocery (already >$150B business)

Most of these are not fully valued today...but they don’t need to be.

So…What does growth look like from here?

If you step back, Amazon is no longer a single business.

It’s a collection of large, compounding engines:

AWS + AI → high-margin, infrastructure-like growth

Ads → margin expansion

Retail/logistics → steady scale + efficiency

New bets → asymmetrical upside

A reasonable way to think about the next 5 years:

Revenue: Could move from ~$700B → $1T+

Margins: Likely expand as mix shifts to AWS + Ads + AI

Free cash flow: Inflects meaningfully post AI investment cycle

The Bigger Insight

What makes this interesting isn’t just growth.

It’s how Amazon grows:

Invest aggressively before returns are obvious

Build infrastructure ahead of demand

Accept near-term pressure for long-term dominance

That’s uncomfortable in the short term.

But historically, that’s exactly where Amazon has created the most value.

Final Thought

Most companies at this scale are optimizing.

Amazon continues to build.

Amazon’s real question isn’t whether it can keep growing...

It’s whether investors are still underestimating how big it can become?

Well, that’s it for today. I hope you enjoyed reading it!

As always, this isn’t a recommendation to buy or sell...it’s about revisiting the process and stress-testing whether the original thesis still holds.

I will see you next week.

Best,

Pooja