Byte # 46: When the Market Puts a Great Business on Sale

Investors often say they want to buy great businesses.

But when the price of those businesses actually falls, hesitation usually increases.

Warren Buffett once made a simple observation:

“Whether we’re talking about socks or stocks, I like buying quality merchandise when it is marked down.”

Yet in practice, the opposite often happens. When markets turn volatile and stocks decline, many investors step aside rather than lean in.

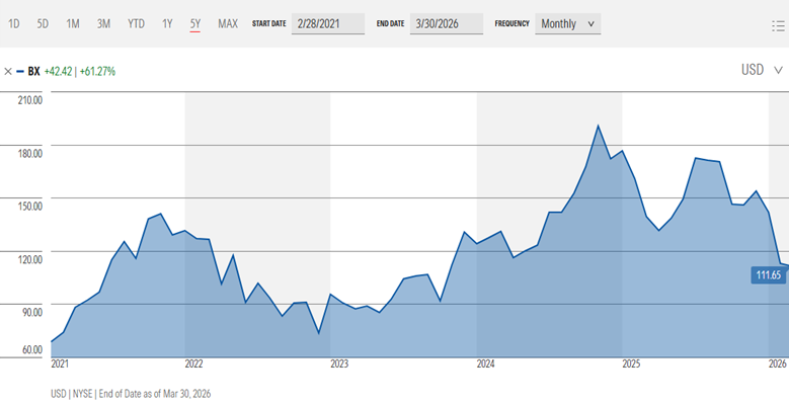

That brings me to a company I have been studying recently: Blackstone. Shares of the world’s largest alternative asset manager have lost ~ 28% of their value so far this year.

This is not to make a recommendation, but to walk through the framework I use when evaluating opportunities.

1️⃣ Market Psychology

When a stock approaches a 52-week low, the natural reaction is to assume something must be wrong.

Sometimes that’s true.

But other times, the decline reflects short-term sentiment rather than a permanent change in the business.

The first question I try to answer is simple:

Has the business deteriorated — or has the market simply become pessimistic?

That distinction matters more than the price movement itself.

2️⃣ Understanding the Business Model

Before thinking about valuation, it helps to understand how the company actually makes money.

Firms like Blackstone operate as alternative asset managers.

They raise capital from institutions and wealthy investors to invest across:

private equity

real estate

private credit

infrastructure

In return, they typically earn:

management fees on assets under management

performance fees when investments perform well

As long as they can continue to attract capital and generate returns, the model benefits from scale and recurring fee income.

3️⃣ The Importance of Asset Growth

One of the key drivers of this model is Assets Under Management (AUM).

Over the past decade, Blackstone has significantly expanded its AUM, benefiting from a broader shift where pension funds and institutions increasingly allocate capital to private markets. Its AUM has increased from $880.9B in 2021 to $1.27T in 2025, a 9.5% CAGR b/w 2021-25.

For investors evaluating the business, the relevant question becomes:

Is the long-term demand for alternative assets still growing?

If the structural trend remains intact, asset managers with strong track records often continue to attract capital over time.

4️⃣ Thinking About Valuation

Finally comes valuation.

Even great businesses can become poor investments if purchased at excessive prices.

Conversely, when strong companies experience periods of weak sentiment, the price investors pay for future earnings may become more attractive.

This is where long-term investors try to separate:

temporary market pessimism from permanent impairment of the business

Blackstone has come under pressure due to private credit redemption fears and a broader macro slowdown in late 2025/early 2026.

At the same time, the underlying business has continued to show scale and earnings power — with ~$1.27T in AUM, Fee Related Earnings growth of ~9%, Distributable Earnings growth of ~19% in 2025, and ~$198B of dry powder for deal acceleration as rates fall - poised for catch-up rally to $170+ targets (+50% upside).

This is where the debate begins as there is a precedent for this kind of volatility.

From its 2021 peak near $150, BX fell ~47% to $71 by late 2022 as the Fed hiked from near-zero to 4.50%, continuing to 5.50% by mid-2023 causing significant pressure across real estate/private market.

The current setup shares some similarities.

Higher Treasury yields (~4.4% on the 10-year) increase financing costs and reduce the relative attractiveness of real estate and credit investments. At the same time, Blackstone’s flagship private credit fund recently posted its first monthly loss amid rising redemptions even though it allowed ~7% outflows versus a 5% limit.

Public high-yield spreads (~330bps) suggest broader markets are not yet pricing in significant stress, but private credit quality has shown signs of deterioration.

What It Means

Taken together: Blackstone could benefit if private credit concerns prove temporary and the rate environment stabilizes.

However, the business remains sensitive to:

higher-for-longer interest rates

pressure in real estate and credit markets

and continued redemption activity

The franchise is strong - but the environment is uncertain.

So the question becomes:

Do you act amid uncertainty, or wait for clearer signals?

Different investors will approach this differently. Some may choose to start small and build positions over time, while others may prefer to wait for more clarity in credit markets.

Studying companies like Blackstone reminds me that investing is not about predicting the next market move.

More often, it’s about understanding the business, the psychology of markets, and the price being asked today.

This isn’t a recommendation to buy or sell - it’s about revisiting the process and stress-testing whether the current investment thesis holds.

Happy Reading and Invest Smart with Pooja 😊