Byte # 30: Food for Thought: Investing in the Backbone of US & Global Markets: SPGI & MSCI

Ladies and Gentlemen,

Today I’m bringing you two compelling stock ideas with deep competitive moats in the Financial Data & Exchanges industry—businesses the world relies on every single day.

Both S&P Global(SPGI) and MSCI Inc. (MSCI) are known as "critical infrastructure" for global investing, providing data, benchmarks, and analytics at the center of capital markets. Despite negative returns year-to-date, the long-term case for owning one or both remains for investors who value structural moats, recurring revenue, and global financialization.

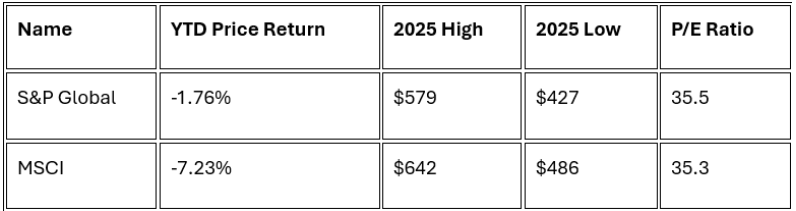

As of today, SPGI's stock price has fallen from its highs near $579 to around $489, and MSCI has dropped from ~$642 to ~$556, both marking negative moves for the year after a strong start.

Performance and Valuation Overview

Make it stand out

Both names continue to trade at elevated P/E ratios, which leaves their stocks sensitive to changes in sentiment, interest rates, or sector flows. Despite beating expectations on earnings and growing revenue, concerns over sector rotation and future growth rates have weighed on both stocks.

Economic Moats and Business Durability

S&P Global operates across ratings, indices, market intelligence, and commodities benchmarks, giving it a diversified, asset-light, and recurring-revenue model with strong pricing power. Its services are deeply embedded in regulatory and workflow systems, creating high switching costs and network effects. EBITDA margins typically exceed 30% with strong cash generation. Its credit ratings division—the world’s largest—is the most profitable segment, while its Market Intelligence business is the largest by revenue, offering data, analytics, desktop solutions, and enterprise tools to financial institutions globally.

MSCI focuses on global indices, factor models, ESG, climate analytics, and portfolio/risk tools. Its moat continues to expand as institutions demand more customized, high-quality data and analytics. Roughly 80% of revenue growth comes from existing clients, highlighting exceptional stickiness and scalability. MSCI’s index segment is its largest and most profitable, supporting ~$17 trillion in benchmarked assets, including over $2.2 trillion in ETFs tied to MSCI indexes. Its analytics segment provides risk and portfolio management software, while its sustainability and climate units supply ESG data. MSCI also serves private markets with real estate benchmarks, reporting, and analytics.

Secular Tailwinds and Compounder Status

Both sit at the center of global themes: passive investing, regulatory transparency, sustainable finance, and risk analytics.

Demand for ESG and climate data, alongside index-linked investing, is expected to grow at double-digit rates through 2030.

Their oligopolistic industry structure supports pricing power and resilience: S&P Global + Moody’s control ~80% of global credit ratings, while MSCI and S&P/Dow Jones dominate indexing.

Valuation and Headwinds

Current Pullback: 2025’s sector rotation and higher rates have pressured high-multiple, fee-based platforms. Investors are reassessing how much future growth is already priced in.

Risks: – Cyclicality in credit issuance (SPGI) – Regulatory scrutiny – Fee pressure and fintech disruption – AI adoption potentially lowering data/analytics barriers to entry.

Valuation: Both trade in the high-30s P/E range—a premium supported by moats and capital efficiency, but a source of volatility if growth moderates.

Financial Strength

SPGI and MSCI both maintain excellent margin profiles—roughly 30%+ and 40%+ respectively—and continue generating strong free cash flow.

S&P Global (Q3 2025):

Record revenue of $3.89B (+9% YOY)

EPS up 24% to $3.86

Solid margins, robust cash flows, consistent buybacks and dividends

MSCI (Q3 2025):

Revenue grew 9.5% YOY to $793.4M

Adjusted EPS up ~19% to $4.25

Strong recurring revenue base, margin expansion, disciplined capital returns

Both companies continue to demonstrate the attributes of long-term “compounders”: predictable cash flow, durable client relationships, and scalable business models.

Food for Thought

Are short-term valuation pressures valid reasons to avoid holding these long-term moats, or an opportunity to build a position into weakness?

Does the trend toward more custom, ESG-driven investment solutions favor one business model more than the other?

Would owning both provide necessary diversification, or simply double down on the “global data backbone” bet?

Both SPGI and MSCI offer rare durability and long-term compounding potential. My personal watchlist includes both, though I currently lean toward SPGI given its greater revenue diversification. That said, I’d love to hear your thoughts and perspectives—your input always helps shape future Bytes!

Wishing you all a wonderful Thanksgiving week and beautiful moments with your friends and family. See you next week! 😊

Cheers,

Pooja