Byte # 27 – How I Built Conviction in a Hidden Energy Gem — Headwater Exploration (CDDRF)

Hello my Friends,

Today, I want to walk you through my investment thesis on Headwater Exploration — so you get an idea of how I build conviction before investing in a particular stock.

Back in March 2025, I came across this company through the Better Investing Stock Screener, which listed top small- to mid-cap growth companies. What caught my attention immediately was its Morningstar Financial Health Grade of A.

Naturally, I wanted to learn more. Here’s a quick snapshot of what the company does:

Headwater Exploration Inc. is an oil and gas exploration and development company focused on onshore operations in McCully Field, New Brunswick, and Marten Hills, Alberta, Canada. The firm generates substantial revenue from selling crude oil, natural gas, and natural gas liquids. It primarily engages in upstream activities — locating and extracting resources — and sells to large refiners and marketers within the Canadian market.

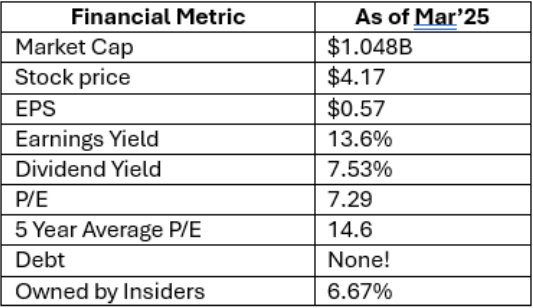

The financials were even more compelling:

This little oil company operates with no debt, holds a strong cash reserve, and boasts both a 13.6% earnings yield and a 7.53% dividend yield.

Honestly, this is probably one of the strongest balance sheets I’ve seen for an oil company — profitable, debt-free, and able to fund growth and dividends without borrowing.

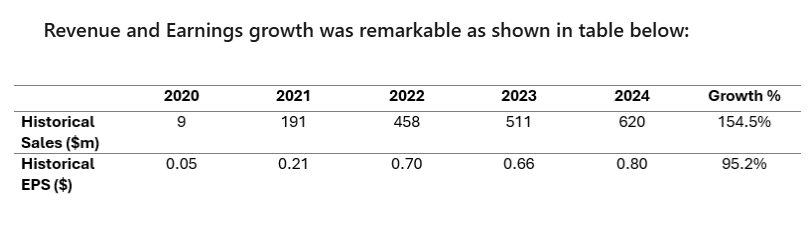

Revenue and Earnings growth was remarkable as shown in table below:

Margins:

Gross Margin: 75.05%

Operating Margin: 42.92%

Profit Margin: 33.12%

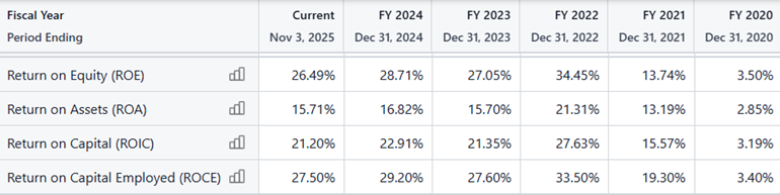

These ratios clearly reflect the management’s strong operational discipline and efficiency — a sign of a well-run company.

What truly differentiates Headwater is its unusually high profitability in the Clearwater Basin. The company keeps production costs extremely low through an innovative and accelerated use of waterflooding, a secondary oil recovery technique. By moving to secondary recovery early, Headwater boosts free cash flow and minimizes long-term costs — a major competitive edge.

Of course, commodity prices remain the biggest risk, but the company appears to be managing that risk quite well via its low production cost technique.

Headwater is now rapidly expanding its waterflood programs, with expectations that by the end of 2026, nearly half of its oil production will come from secondary recovery. This will make its production profile more predictable and cost-efficient — a big plus for long-term investors. Also, production and cash flow growth should remain robust even with weaker commodity prices.

Another interesting fact: its Enterprise Value (EV) is actually lower than its Market Cap. Since EV = Market Cap + Debt – Cash, and the company has no debt, this implies that an investor could theoretically acquire the company for less than the value of its assets — an interesting scenario.

As of now, the stock trades at $5.28, and in its Q3 2025 earnings release, management announced:

“Fourth quarter production is expected to average 23,500–24,000 boe/d, representing a year-over-year increase of 11%. Annual production guidance is increasing to 22,600 boe/d from 22,250 boe/d. This production growth will be achieved with 33% fewer development wells and $35 million less capital than originally budgeted — thanks to exceptional results and a sustainable downward trend in well costs.”

I hope this gives you a sense of how I build conviction before investing — it’s less about finding the next big thing and more about understanding the fundamentals that truly make a company stand out.

My take: Keep this one on your radar — and if the market offers a dip, it might just be worth a closer look.

Your best friend in investing 😊

Pooja