Byte #22 – Intuitive Surgical (ISRG): Growth, Risks, and Why I’m Investing

Dear Friends,

Last week, I wrote about the importance of reviewing MD&A (Management Discussion & Analysis) and mentioned I’d be walking through this document for Intuitive Surgical, Inc. (“ISRG”).

Let’s start with what the company does.

Intuitive is a global leader in medical technology, best known for its robotic-assisted surgical systems. Its flagship product, the da Vinci Surgical System, enables minimally invasive surgery by combining advanced robotics with computer-assisted technology. Complementing this is the Ion endoluminal system, designed for minimally invasive lung biopsies.

The company has a strong global footprint across the U.S., Europe, and Asia, and its products feature multiple da Vinci models offering high-definition 3D vision and precision tools. Intuitive also operates under a classic “razor-and-blades” model, generating recurring revenue through instruments, accessories, and services tied to its installed base. With nearly 10,000 da Vinci systems placed worldwide, the company benefits from an extensive procedure database and a wide economic moat.

On September 12, 2025, Intuitive introduced real-time surgical insights for da Vinci 5, which boasts over 10,000x the computing power of its predecessor, the da Vinci Xi—marking a huge leap forward in surgical robotics.

Now, that you know a bit about the company, I looked into its latest MD&A from 10-Q | Quarterly report for Q2 dated Jul 22nd 2025, and here are the key takeaways:

Revenue grew 21% YoY to $2.44 billion, driven by higher system adoption and procedure volumes.

GAAP net income rose to $658 million ($1.81 per share), up from $527 million ($1.46) in Q2 2024.

The installed base grew 14% to ~10,500 systems, including 180 da Vinci 5 units.

Procedure volume rose 17% globally, especially across multiport and SP platforms.

R&D spend increased 12% to $313 million, supporting innovation and talent growth.

Da Vinci 5 rollout gained approvals in Europe and Japan for both adult and pediatric use.

Force feedback technology was introduced as a breakthrough, enhancing surgical precision.

Operational priorities included supply chain optimization and manufacturing scalability.

The company ended the quarter with $9.5 billion in cash and investments and zero debt.

CEO Dave Rosa emphasized a continued focus on innovation, digital tools, and patient outcomes.

These points highlight Intuitive’s strong growth, financial resilience, innovation pipeline, and expanding global reach.

Risks and Competitive Landscape

While Intuitive has maintained leadership, it no longer holds a monopoly. Management highlighted:

U.S. customers are focusing more on utilizing existing systems rather than expanding capacity.

China’s demand faces headwinds from domestic competitors and regulatory campaigns.

Future placements could be influenced by supply chain risks, economic/geopolitical uncertainty, inflation, and high interest rates.

Competition from alternative surgical and diagnostic technologies remains significant.

Key competitors include:

Medtronic (Hugo system, leveraging global presence).

Johnson & Johnson (Ethicon/Auris Health) with its Monarch platform.

Stryker, expanding its robotic offerings beyond orthopedics (Mako system).

Why I Invested

For me, the deciding factor is recurring revenue. Roughly 85% of Intuitive’s total revenue comes from recurring sources—sales of instruments, accessories, and digital services tied to its installed base.

Recurring revenue trends:

2022: $4.92B (79% of revenue)

2023: $5.94B (83%)

2024: $7.04B (84%)

This high-margin, predictable cash flow not only provides stability but also funds innovation and growth initiatives. With a growing installed base and rising procedure volumes, Intuitive’s recurring revenue stream forms the backbone of its financial strength.

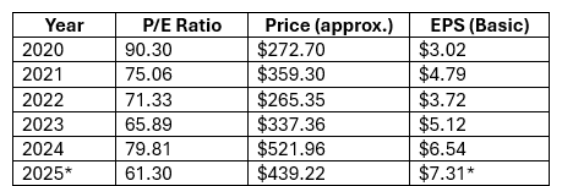

Valuation Snapshot

Current share price: $430–$495

Market cap: ~$157B

P/E ratio: ~61, well above market average

*2025 data is as of today with mid-year earnings estimates

As one analyst put it:

“While the valuation is elevated, Intuitive has consistently justified its premium through superior growth and profitability. With scale, market leadership, and decades of growth ahead in an under-penetrated global market, it remains a compelling long-term investment.”

Closing Thoughts

In my view, Intuitive Surgical represents a high-quality compounder supported by recurring revenue, strong innovation, and global demand for minimally invasive surgery. Despite premium valuation and competitive pressures, I see it as a solid long-term investment.

These were the key deciding factors behind my investment. Of course, there are many other financial metrics and considerations that go into a final decision, which I haven’t covered here.

If you want more perspectives, I encourage you to check out this article from Forbes, which discusses recent developments and market activity around ISRG stock: “Intuitive Surgical: What’s Happening With ISRG Stock” (Forbes)

I hope you found this byte insightful. My goal is to keep things simple, educational, and to the point.

Thank you for reading and subscribing!

Best,

Pooja